Roku’s strong Q2 2023 results sent its stock soaring. But the ebullience could fade quickly in the second half due to problems with ARPU, profitability, and the strikes.

Roku beat Wall Street expectations in Q2 2023. It delivered an 11% year-over-year growth in revenue, earning $847 million versus an expected $774. Active accounts also grew well, increasing by 1.9 million to 73.5 million. The company lost active accounts in Q2 2022. Most revenue growth came from Roku’s Platform business, which grew by 11% to $744 million. Stock traders cheered the results pushing the stock 31% higher to finish the day just below $90 a share.

Roku beat Wall Street expectations in Q2 2023. It delivered an 11% year-over-year growth in revenue, earning $847 million versus an expected $774. Active accounts also grew well, increasing by 1.9 million to 73.5 million. The company lost active accounts in Q2 2022. Most revenue growth came from Roku’s Platform business, which grew by 11% to $744 million. Stock traders cheered the results pushing the stock 31% higher to finish the day just below $90 a share.

The good Q2 2023 results underline Roku’s strong position in the North American market, where it dominates the TV OS market. However, there are some major clouds on the horizon for the company. ARPU growth is stagnant, it is underestimating the negative impact of the strikes, and profitability is drifting lower. Here are the dimensions of each problem for the company and what executives say about it.

No growth in ARPU

With three consecutive quarters of no or declining ARPU growth, the company offered this explanation in the Shareholder Letter:

“This decline was due to strong global Active Account growth outpacing Platform revenue growth.”

It is reasonable to expect new Roku users to watch less as they become oriented to the platform. However, there are reasons this statement is a less than satisfactory explanation.

It is reasonable to expect new Roku users to watch less as they become oriented to the platform. However, there are reasons this statement is a less than satisfactory explanation.

Vizio, which has a very similar business model to Roku, is facing the same advertising headwinds as Roku, yet it did not see any pullback in ARPU growth. In Q4 2022 and Q1 2023, the company delivered 2% and 3% growth in ARPU. Over the same period, it also grew active users by 5%, slightly less than Roku’s 9% active account growth.

And Roku’s historical performance does not support the idea that strong account growth results in weak ARPU progress. For example, between Q3 and Q4 2021, Roku grew active accounts by 7% or 3.7 million, and ARPU increased by 2%.

This data suggests something else is going on to retard ARPU growth. The most likely culprit is the Media and Entertainment (M&E) spending pullback.

Underestimating the impact of the strike

Roku expects the writers’ and actors’ strikes to impact its performance negatively. Charlie Collier, President of Roku Media, offered this assessment of the Q3 and Q4 performance:

“We do expect M&E to be pressured in H2, which is why we expect a tick down in platform gross profit for Q3.”

The company says revenue and gross profit in Q3 2023 will come in slightly below Q2 levels, whereas in the past, both have increased between Q2 and Q3.

Mr. Collier also downplayed the longer-term impact of the strike on Roku:

“There is a huge amount of content here, so people will have no problem finding something to watch.”

However, Roku heavily depends on M&E revenue and the flow of new content that sustains it. Anthony Wood, Roku’s CEO, characterized M&E as their core business. M&E clients buy a lot of advertising space on Roku to promote their new shows and movies. As the writers’ and actors’ strikes begin to bite, the flow of new content requiring promotion will slow to a trickle.

M&E clients also provide significant revenue for Roku in other ways, according to Mr. Wood:

“We generally get rev shares for billing and signing up new subscribers in that category.”

Again, new sign-ups will likely decline sharply as the strike drags on, and cancelations will grow as new content dries up.

Mr. Collier says that Roku is diversifying away from M&E. For example, he says consumer packaged goods (CPG) and Health and Wellness show “green shoots.” But those green shoots will not grow fast enough to fill the void caused by the pullback in M&E if the strikes go on for an extended period.

Falling profit margins

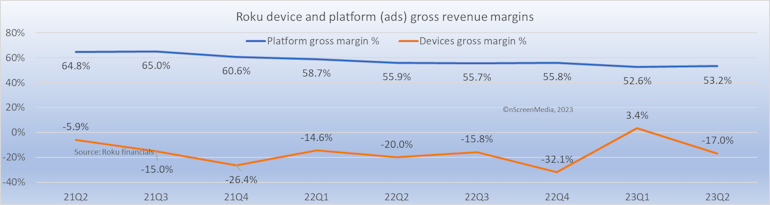

Finally, Roku is seeing profit margins fall in both its core businesses. Device sales returned to heavy losses in Q2, with gross profit margins plummeting to -17%. Roku has made money on device sales in only one of the last nine quarters, with an average loss of -16%. Entry into the TV business will likely exacerbate device losses. Of course, as Mr. Wood reminded us in the Q2 earnings call, device sales are a loss leader for the far more profitable ad-drive Platform business. But the question is, how low is Roku prepared to let device losses go?

Unfortunately, the Platform business is also becoming less profitable. Its gross profit margin has been drifting lower for the last two years. In Q2 2021, it was 64.8%, and in the quarter just ended, it settled at 53.2%.

Roku is not alone in the trend toward lower profit margins. Vizio is also seeing the same thing. However, it is maintaining a breakeven or slight profit on device sales, and its ad-driven Platform+ reported a 59% gross profit margin in Q1 2023. Hopefully, both will improve as the ad market recovers and the strikes reach an amicable conclusion.

At nScreenMedia, we never accept payment to publish an opinion piece. However, we do accept general site sponsorship, though sponsors exert no editorial influence over our conclusions and opinions. That said, we are grateful for their patronage. Please join them. For other important disclaimers and how you may use nScreenMedia materials in your work, visit https://nscreenmedia.com/about/disclaimer/.

![]()

![]()

![]()

![]()

![]()

![]()